The latest edition of our monthly Australian Energy & Environmental Market Update is now available. Keep reading for energy and environmental price movements, policy updates and other news.

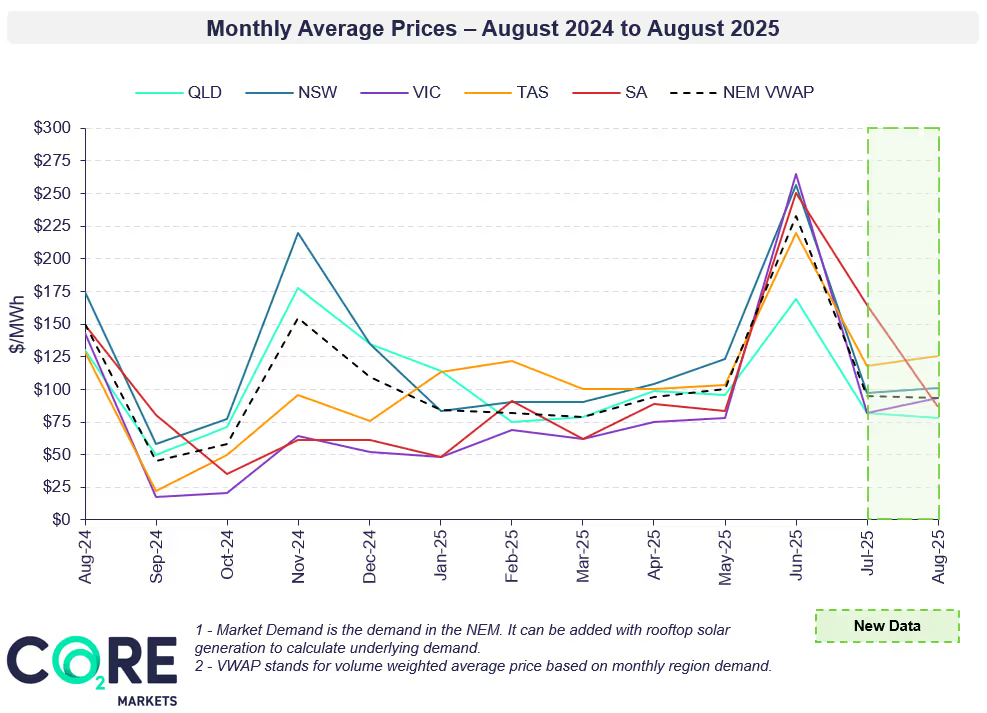

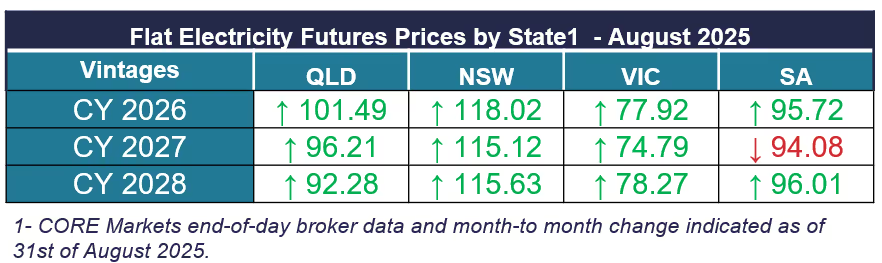

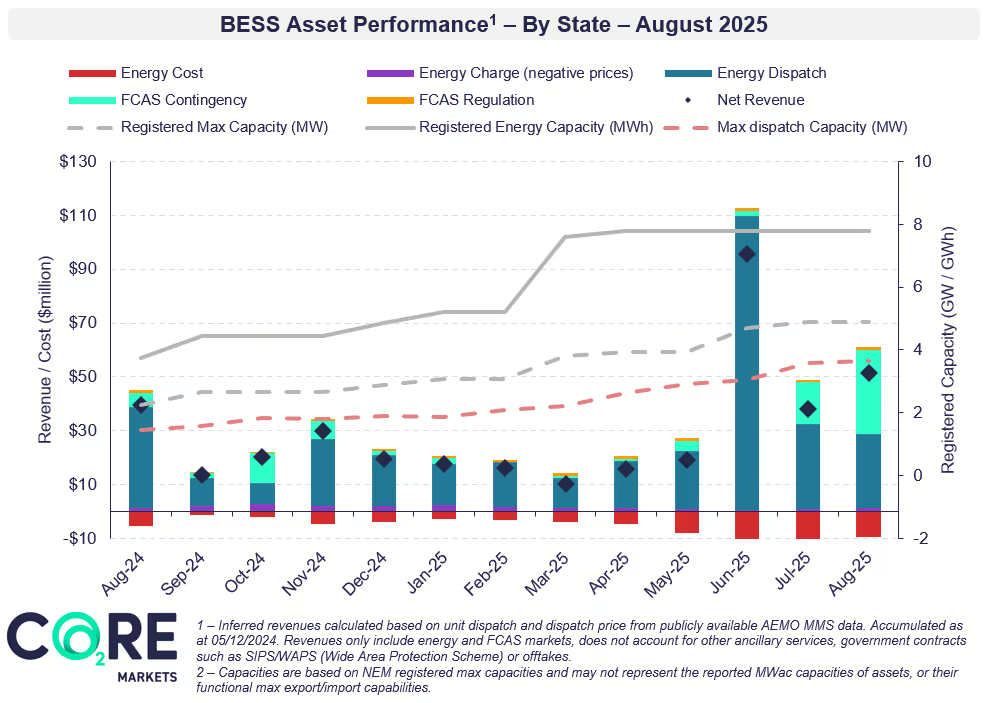

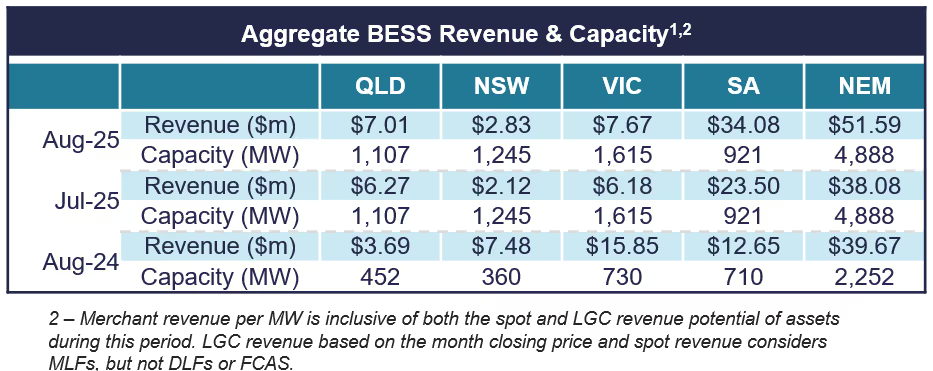

This month’s update covers August’s spot market movements, with NEM-wide volume-weighted average prices continuing to soften, down 2% from July to $93.16 /MWh. SA led the decline with prices nearly halving month-on-month, while TAS recorded the highest regional price at $125.23 /MWh, underpinned by continued low wind and hydro output driving up gas-fired generation. BESS revenue strengthened compared to July, driven by a surge in FCAS revenue up 91% across the NEM.

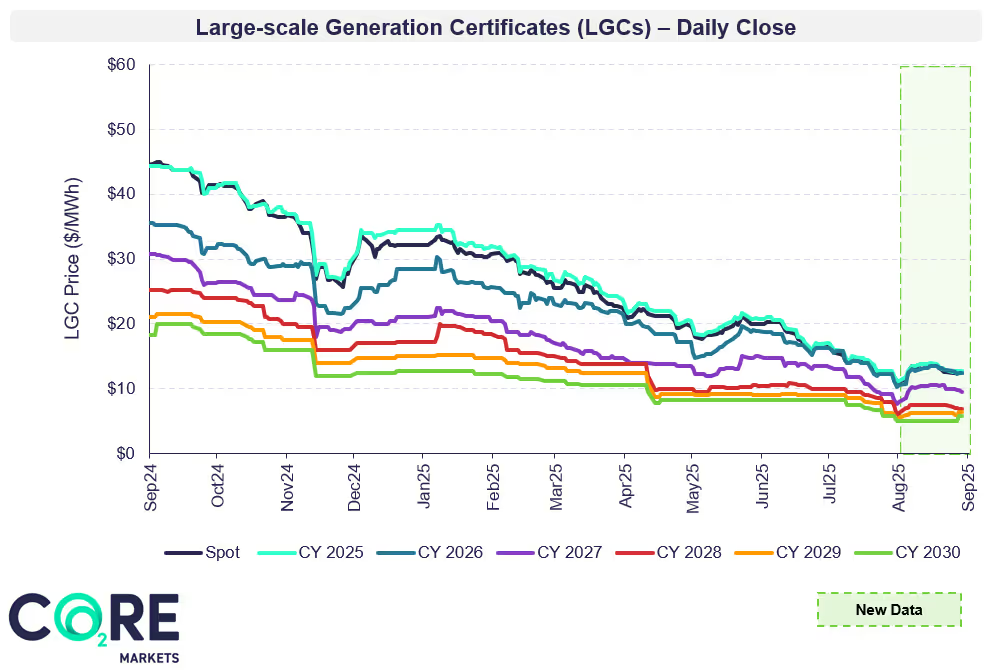

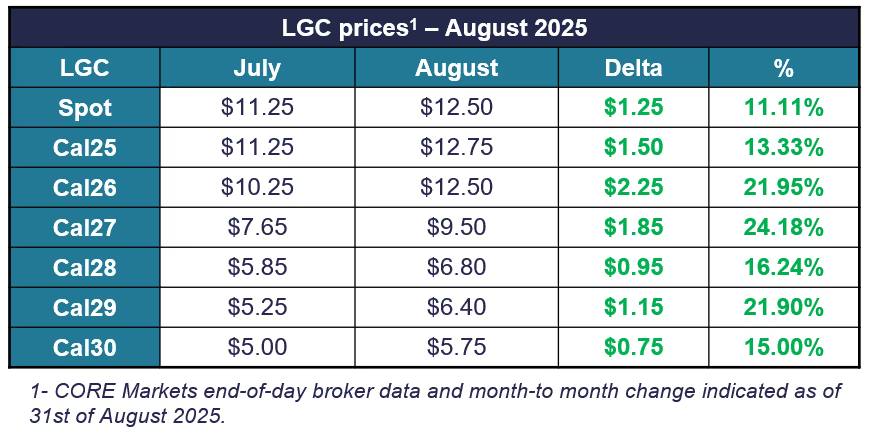

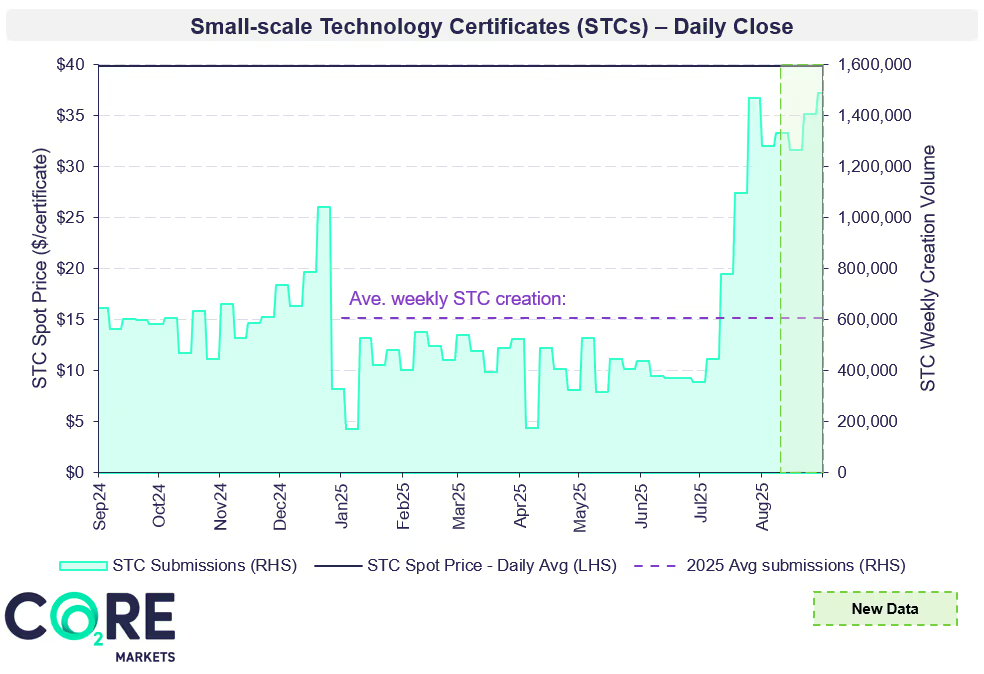

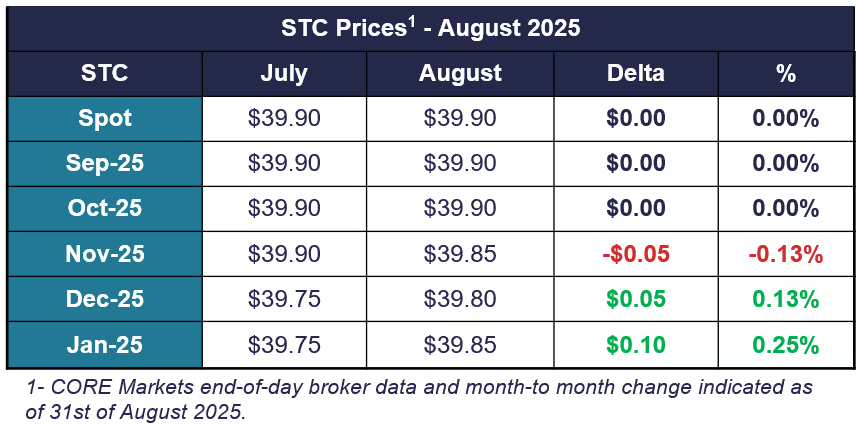

In the environmental markets, LGC prices showed a more stable spot-level beginning to emerge ~$1/MWh above the floor. STC issuances remained strong following the Cheaper Home Batteries Program, and forward trading remained active and stable across the near-dated tenors. Key policy and market developments this month include the release of the NEM Review draft report, AEMO 2025 ESOO, and the AER Q2 report. In other news, this month’s update covers Engie’s landmark virtual battery deal with AGL and the start of the Waratah BESS SIPs contract.

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

NEM-wide variable Renewable Energy (VRE) penetration increased by 1.35 percentage points from last month now sitting at 41.28%. This increase was mainly driven by an uptick in rooftop solar generation across the NEM.

Each month we feature a different asset type - rotating between coverage of solar, wind and BESS projects. This month's focus is BESS asset performance.

Looking for more in-depth renewables asset analysis?

Learn more about our Renewable Energy Offtake Market Report, an important and recurring pulse check for renewable energy buyers and seller.

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

The STC Clearing House has once again remained in surplus, aided by consistent weekly submissions above >1mil certificates.

The first government Battery Small-scale Technology Certificate (BSTC) purchase (~200 STCs) has occurred, but further action is awaited and much anticipated.

Forward trading remains active and stable across the near-dated tenors in the wake of issuances skyrocketing in recent weeks. Which came off the back of the Cheaper Home Batteries Program (CHBP) implementation.

Looking for ACCU coverage? Read our ACCU Market Monthly Report here.

This month, the energy market continued to soften from the June’s high, with spot prices easing slightly and futures stabilising following late-July declines. SA recorded the steepest drop, while TAS experienced elevated pricing due to continued low wind and hydro output. Battery asset revenue increased in August, driven by FCAS revenues surging across the NEM.

For asset owners and market participants, understanding key seasonal trends in the market highlights the importance of strong market knowledge and effective hedging strategies to manage the impact of seasonal variations and maximise revenue opportunities.

The CORE Markets team partners with renewable energy developers and corporate buyers to manage market risks. Get in touch to explore how we can support your energy market approach.

The LGC market showed a more stable spot-level beginning to emerge ~$1/MWh above the floor. STC creation remained strong, underpinned by the Cheaper Home Batteries Program, while forward market activity remained active and stable.

Regulatory changes in the ESC market are expected to tighten future supply, driving recent price volatility. Keeping ahead of regulatory and policy developments is key to navigating these markets and aligning procurement strategies with evolving risks and opportunities.

The CORE Markets team supports demand and supply side market participants in navigating these markets – across strategy, procurement and trading execution. Get in touch to learn how we can support your goals.

The events outlined in this month's update highlight the evolving nature of energy and environemental markets and the complexity of the net zero transition.

To discuss your unique requirements, get in touch with our team today to see how we can help.

Australian Energy & Environmental Market Update - August 2025

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.