As the Australian federal election approaches in May 2025, carbon market participants are facing an exciting yet uncertain phase. We explore four potential election scenarios and key upcoming milestones for Australian carbon market fundamentals.

Reading time: 8 min

As the Australian federal election approaches in May 2025, carbon market participants are facing an exciting yet uncertain phase. The election outcome could significantly impact the regulatory landscape, carbon pricing, and emissions reduction policies.

For corporates and other participants in the Australian carbon market, particularly those covered by the Safeguard Mechanism, understanding these potential changes is crucial for strategic planning and compliance.

In this article, we explore:

This article contains select insights usually exclusively available to our Carbon Intelligence Package subscribers.

Learn more about the Carbon Intelligence Package - a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

Within the context of the shifting ACCU supply landscape and the review of the Safeguard Mechanism scheduled for FY2027, the outcome of the upcoming federal election will be important for the market over the remainder of the decade.

Three of the four possible election outcomes – namely, a Labor minority, Coalition minority or a Coalition majority – could promise material impacts to both supply and demand side of the ACCU market.

Below, we consider potential outcomes to the market based on the makeup of the House of Representatives for the next term of government.

Scenario 1: Labor Minority – Hung Parliament

Scenario 2: Labor Majority

Scenario 3: Coalition Minority – Hung Parliament

Scenario 4: Coalition Majority

The AFR – Freshwater Strategy Poll (as updated on the 30th of March) predicted a Labor minority government as the likely election outcome.

Based on this scenario, we outline below five key scheme, legislative and regulatory settings that could be considered for amendment as a result due to increased independent and minor party voices in Parliament.

In the event of a minority government, the levers that would require legislative amendment could be significantly harder to enact due to the diversity of voices in the House of Representatives.

Regulatory reforms however can generally be made through ministerial discretion and would therefore be less cumbersome to enact.

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

Beyond the election, several key factors will shape the future of the Australian carbon market.

These include the growth in Safeguard Mechanism Credit (SMC) volumes, updates to Australian Carbon Credit Unit (ACCU) methodologies, and other upcoming changes.

Understanding these elements is crucial for market participants.

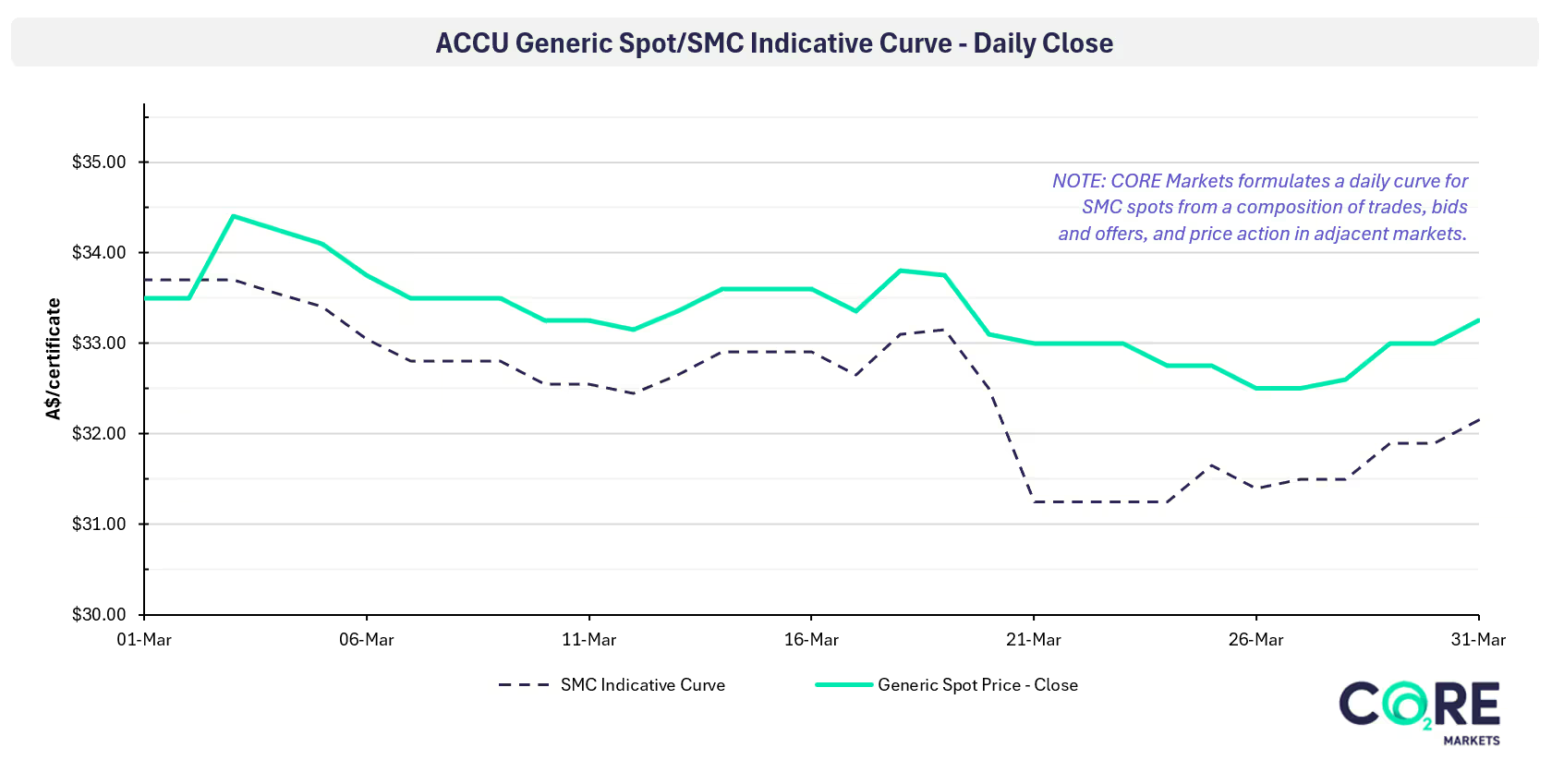

SMCs are tradable certificates that can be used to offset unavoidable emissions for Safeguard liable entities. They’re created by entities that emit below their Safeguard Mechanism baselines. SMC can be banked for future use, meaning if an entity generates SMCs today and expects liability to grow in the future, they can be held and retired later. SMCs incentivise emissions reduction by putting a price on reduction efforts, and those who generate more today can create a new revenue source.

The Clean Energy Regulator issued the first SMCs in the new registry in February.

CORE Markets facilitated the first ever SMC trade on February 27, broking the first trade parcel of 190,000 units at $34.00 – $0.70 below the generic ACCUs traded the same day.

As we approached the 31 March 2025 compliance deadline, the demand for SMCs slowed down as most Safeguard facilities had acquired all the units they needed for compliance purposes. Policy uncertainty also kept SMC trading activity at subdued levels ahead of the election.

Following the first SMC trades, interest has been sparked for forward SMC deals. More activity in the SMC market is anticipated in the months to come as the market continues this initial price discovery phase. We expect the units to continue to sit in the range of $0.50-$0.70 discounted to spot Generic or Generic No AD ACCUs.

SMC issuance volumes, demand volumes, and prices paid for the new units, could have a significant bearing on demand for ACCUs.

For live updates on the SMC market including upcoming in-depth analysis, explore our Carbon Intelligence Package.

With 19 methods due to sunset within the next 12 months, representing 8% of active projects, the government has prioritised four new methods to lift constraints in the supply pipeline.

The Department of Climate Change, Energy, the Environment and Water (DCCEEW) published a plain-English draft of the Integrated Farm Land Management (IFLM) method, which will allow land managers to generate ACCUs for multiple carbon management activities on a single property.

This new method will include activities previously eligible under the expired Human-Induced Regeneration (HIR) method, which constitutes a large portion of ACCU supply.

These updates enhance the credibility of ACCUs, boost market confidence, and introduce new compliance requirements. They also diversify project types, affecting supply and demand dynamics, and encourage innovation in carbon abatement techniques.

However, with the exposure draft delayed to the second half of 2025, the significant delay in method development becomes a constraint to increasing participation in the ACCU market and the short-term supply of credits.

For further analysis of Carbon Abatement Contracts, including projected ACCUs in the CCM and CCM price, explore our Carbon Intelligence Package.

In the face of regulatory changes and other upcoming market shifts, staying well-informed is crucial for all carbon market participants or carbon market exposed entities.

Carbon insights are increasingly needed for daily decision-making, such as managing commercial and supply risks, identifying project credentials, informing project planning and executing trading opportunities.

Created by our award-winning carbon team with over 20 years of in-market expertise, the Carbon Intelligence Package offers extensive and detailed market insights, cutting-edge financial and physical data, advanced analytical tools and access to market experts.

Explore the package here or get in touch to connect with one of our carbon experts.

Election 2025 and beyond: Key changes shaping the Australian carbon market and Safeguard Mechanism

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

CORE Markets has launched Asset Intelligence, connecting renewable project data with power market context, commercial analysis, forecasting and risk modelling to support stronger asset and portfolio decisions.

CORE Markets has launched Asset Intelligence, connecting renewable project data with power market context, commercial analysis, forecasting and risk modelling to support stronger asset and portfolio decisions.