The latest edition of our monthly Australian Energy & Environmental Market Update is now available. Keep reading for energy and environmental price movements, policy updates and other news.

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

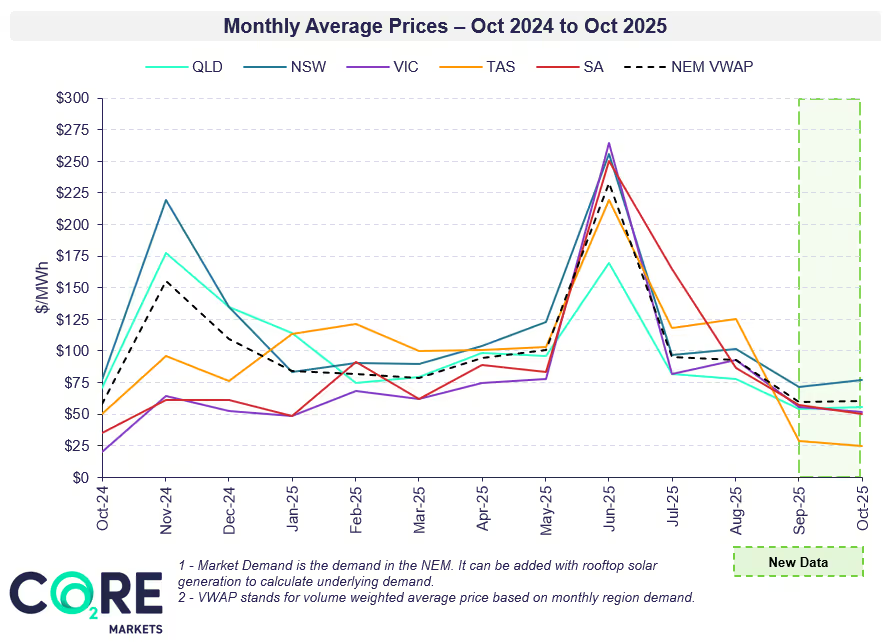

NEM-wide variable Renewable Energy (VRE) penetration increased 0.25 percentage points from last month, reaching 41.79%. This growth was mainly driven by higher rooftop and utility solar generation, typical for the spring season.

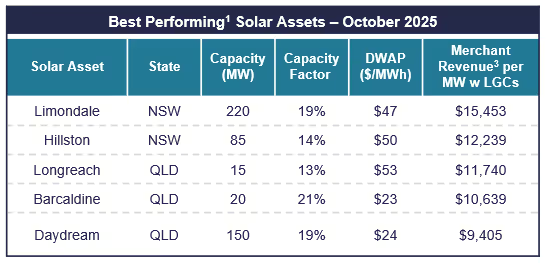

Each month we feature a different asset type - rotating between coverage of solar, wind and BESS projects. This month’s focus is solar asset performance.

Looking for more in-depth renewables asset analysis?

Learn more about our Wholesale Energy and Offtake Market Report, an important and recurring pulse check for renewable energy buyers and seller.

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

Looking for ACCU coverage? Read our ACCU Market Monthly Report here.

Log in to the CORE Markets platform for more market data, insights and commentary. Don’t have an account? Learn more

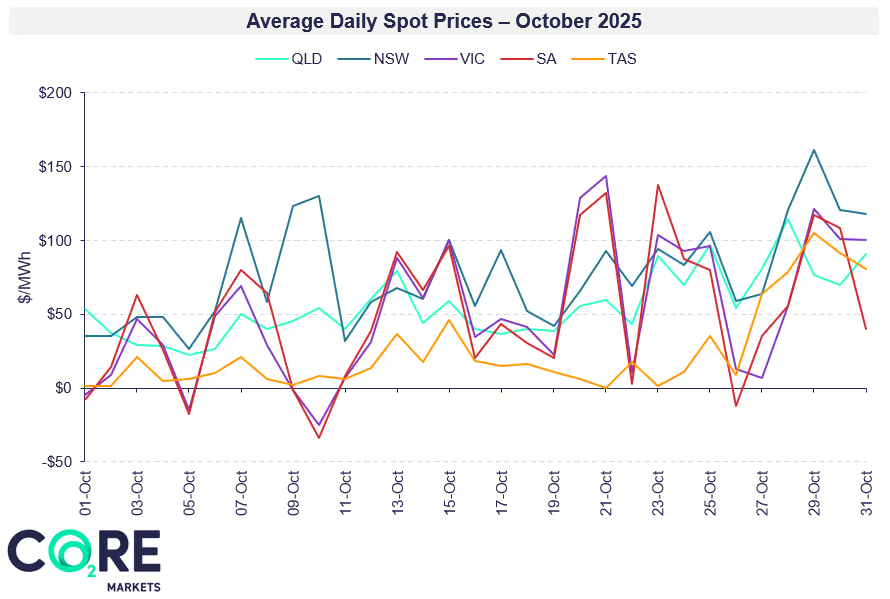

Subdued wholesale pricings highlights risks for sell-side spot market exposed entities. Asset owners may rely on PPAs, swaps, firm blocks, and other offtake mechanisms to manage volatility. The lower merchant revenues for renewable energy projects could also prompt LGC sell-offs as cash flow is managed during spring.

For buyers, these conditions create an opportunity to secure contracts and hedge ahead of likely summer price increases. Strong solar output in NSW and QLD reinforces the importance of regional performance insight when shaping procurement or investment strategy.

These dynamics are explored in CORE Markets’ Wholesale Energy and Offtake Market Report, which outlines current contracting structures, price signals and risk management approaches across the renewable energy market.

The CORE Markets team partners with renewable energy developers and corporate buyers to manage market risks. Get in touch to explore how we can support your energy market approach.

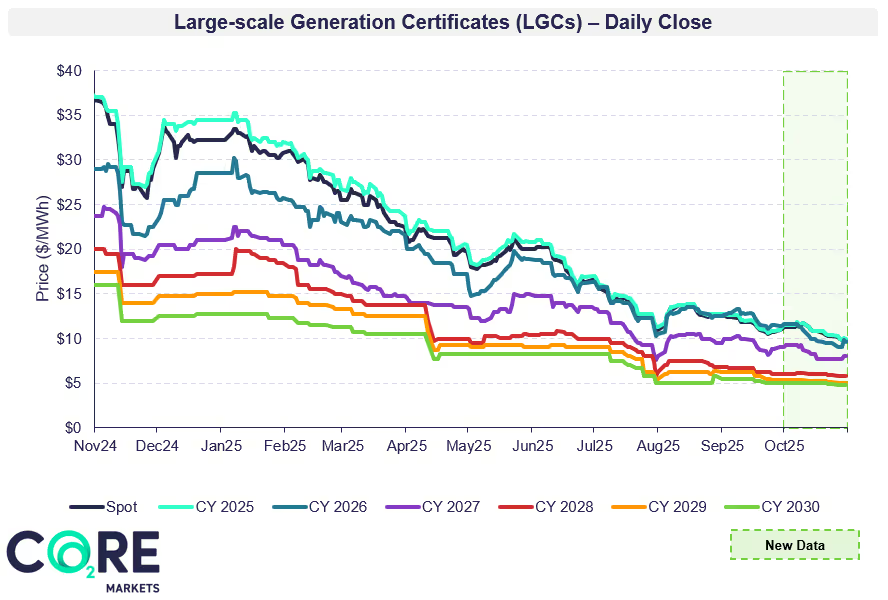

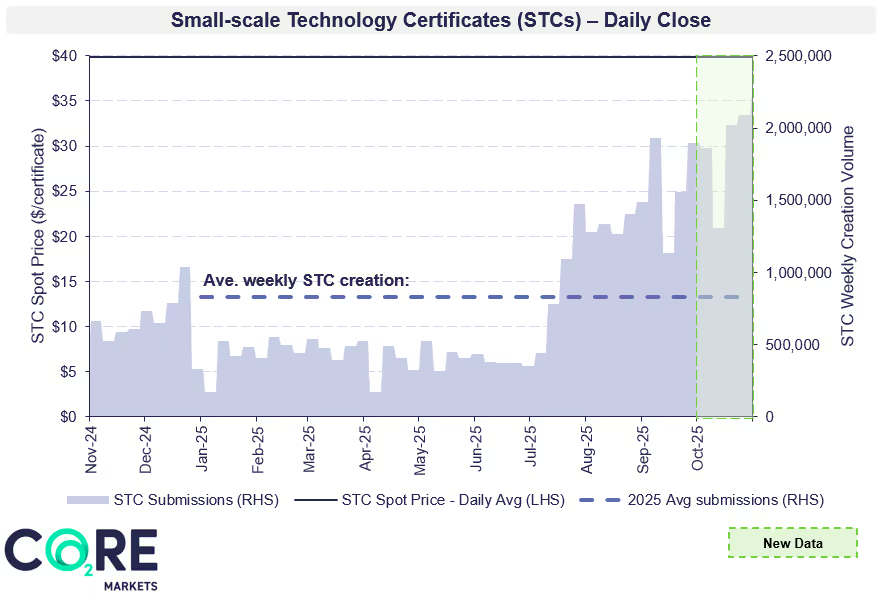

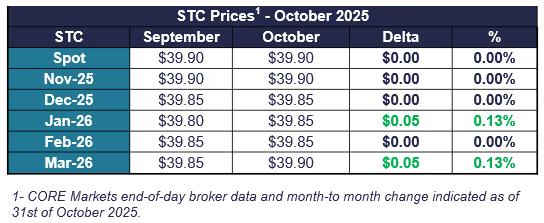

LGC prices continued to ease through October as surplus supply remains priced into 2030, while STCs stayed firm on strong creation under the Federal Battery Rebate Scheme. VEEC and ESC markets remain active, with participants watching new activity types and tightening supply pipelines ahead of next surrender deadlines. The sharp PRC target cut has constrained creation opportunities and dampened confidence in new project activity.

Staying ahead of these regulatory and pricing shifts will be key to optimising procurement and managing compliance costs.

The CORE Markets team supports demand and supply side market participants in navigating these markets – across strategy, procurement and trading execution. Get in touch to learn how we can support your goals.

The events outlined in this month's update highlight the evolving nature of energy and environemental markets and the complexity of the net zero transition.

To discuss your unique requirements, get in touch with our team today to see how we can help.

Australian Energy & Environmental Market Update - October 2025

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.