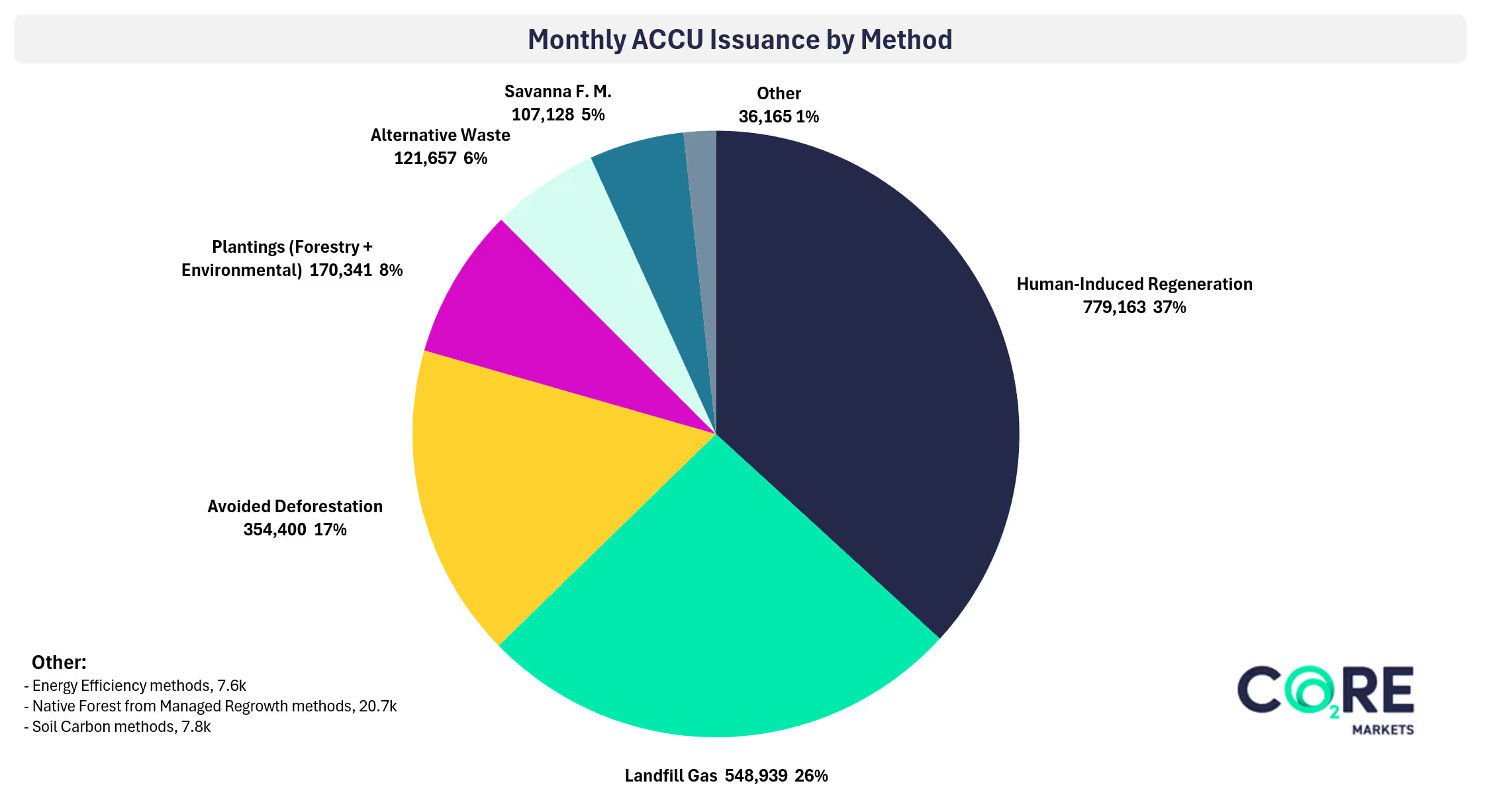

This report provides an overview of the month’s Australian Carbon Credit Unit (ACCU) market activity along with key developments and milestones.

This report provides an overview of the month’s Australian Carbon Credit Unit (ACCU) market activity along with key developments and milestones.

Please note: Our in-market team produces daily and detailed updates and trade reports to CORE Markets software subscribers and clients. Contact us to find out more.

Looking for more carbon market activity and policy coverage?

Learn more about our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

For more data and market commentary, explore our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

For more data and market commentary, explore our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

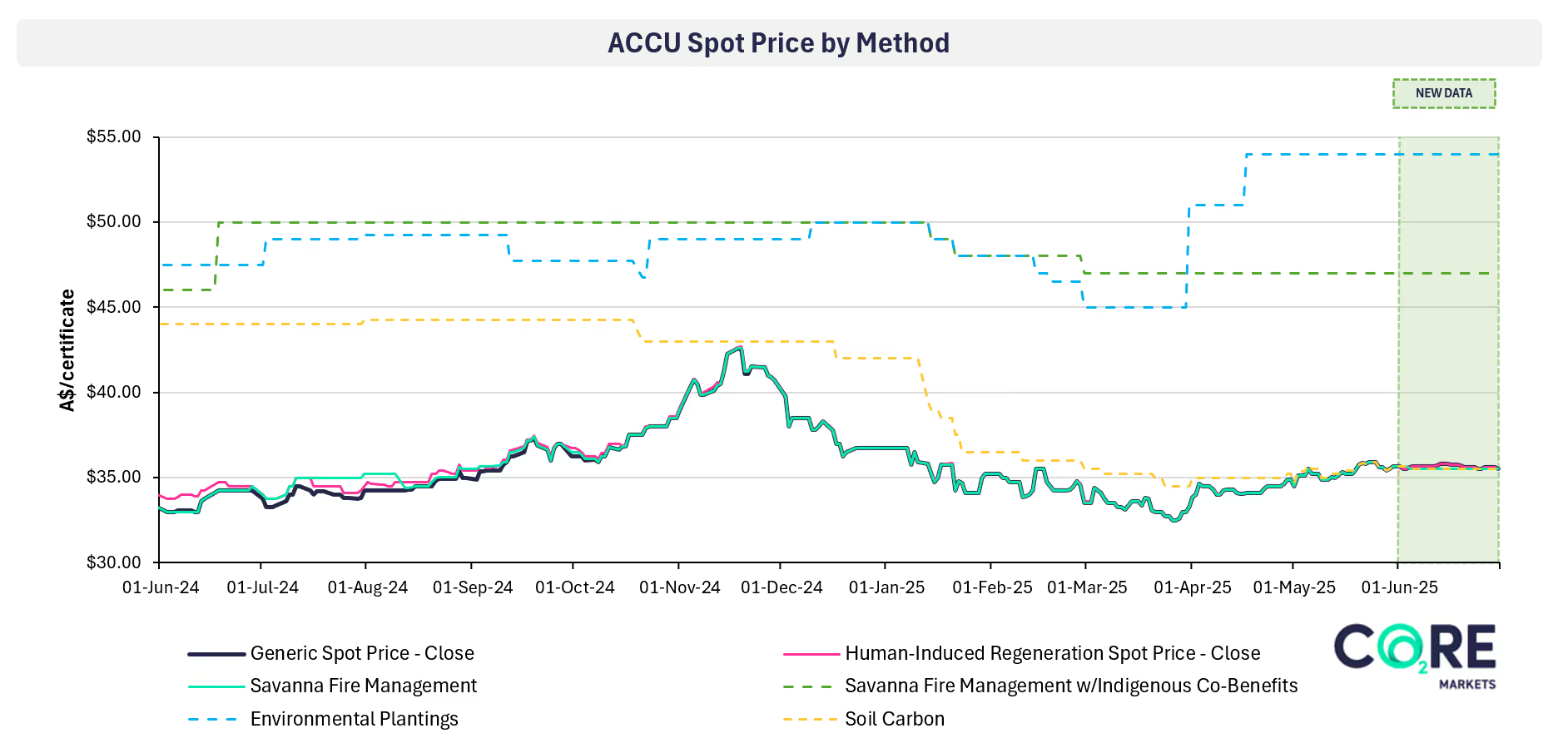

To help market participants better model their commercial position, the CORE Markets team has developed a unique method-specific ACCU price forecast.

We believe demand preferences will vary among buyer groups, the costs of developing new ACCUs will vary by methodology and that this will be reflected in the market for the foreseeable future.

The CORE Markets ACCU price forecast is created by our environmental markets advisory team with data from our carbon analytics platform.

The model is continuously tested and refined with the help of an expert industry working group.

In addition to the base model, the CORE Markets team can provide a full suite of scenario analysis forecasts on a bespoke basis.

Available exclusively to Carbon Intelligence Package subscribers. Learn more

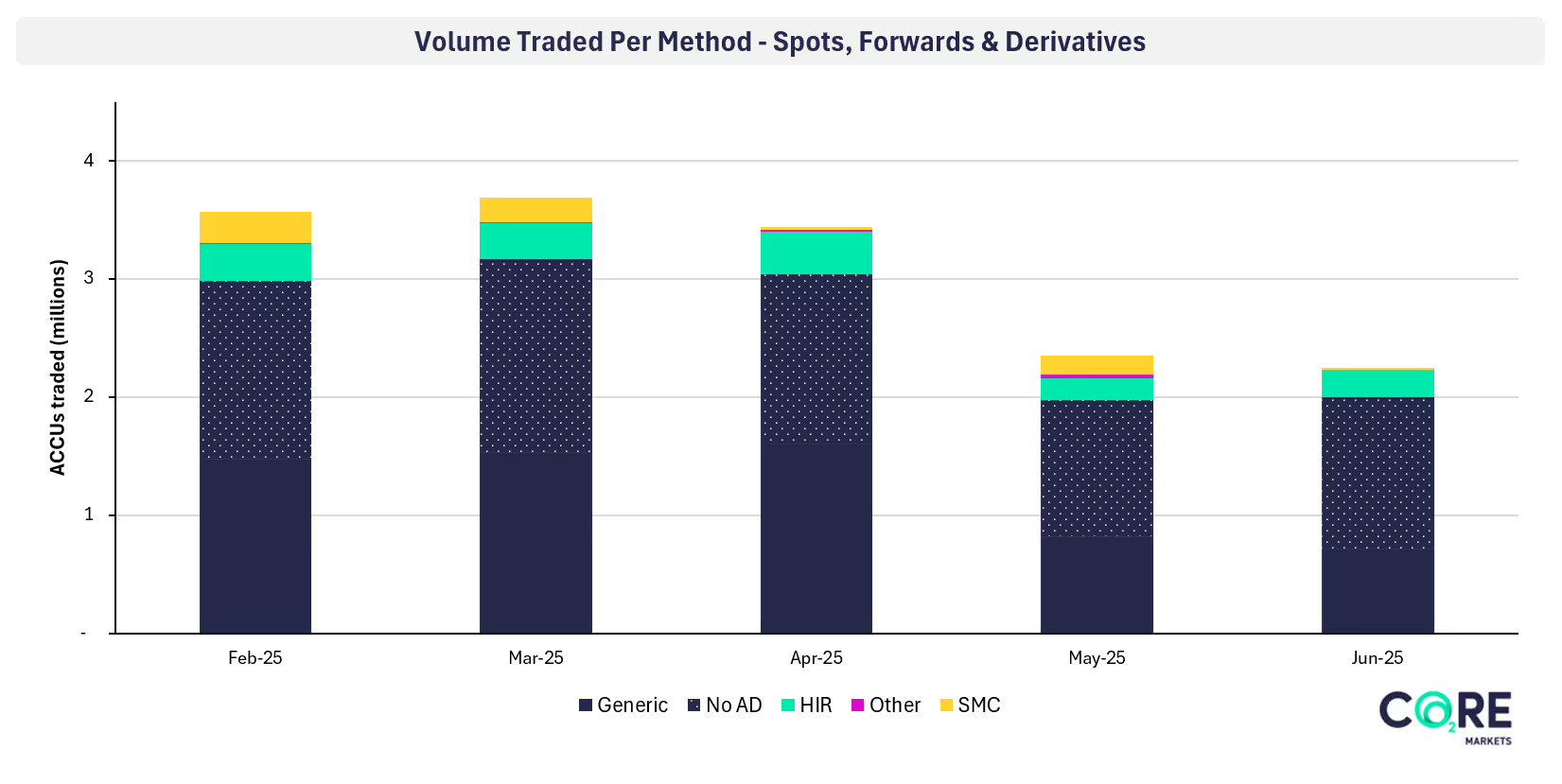

ACCU demand trends are considered in detail in our monthly analysis as available to Carbon Intelligence Package subscribers.

This includes:

Learn more about the Carbon Intelligence Package

For commentary on Carbon Abatement Contracts and the projected volumes of ACCUs in the Cost Containment Mechanism, explore our Carbon Intelligence Package - a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

ACCU supply trends are considered in detail in our monthly analysis as available to Carbon Intelligence Package subscribers.

This includes:

Learn more about the Carbon Intelligence Package

ACCU Market Monthly Report - June 2025

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

.jpg)