This report is published monthly and provides a high-level overview of the key developments in select compliance and voluntary carbon, and Sustainable Aviation Fuel markets.

This report is published monthly and provides a high-level overview of the key developments in select compliance and voluntary carbon, and Sustainable Aviation Fuel markets.

*Please note: This report is produced using select data, commentary and insights as available in full to our Carbon Intelligence Package subscribers.

Learn more about our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

ACCU prices edged higher in September despite sharp two-way trading around major policy announcements. Generic and No Avoided Deforestation (No AD) spot ACCUs closed A$0.40 higher at A$37.30, after briefly surpassing the A$38.00 resistance level mid-month - their highest point since December 2024.

Prices retreated following the release of Australia’s 2035 Nationally Determined Contribution (NDC), which set a 62–70% emissions reduction target below 2005 levels, before recovering into month-end.

Human-Induced Regeneration (HIR) units tracked the broader market, closing level with Generic and No AD ACCUs. HIR trading increased slightly, accounting for 12% of total activity (430,000 units) compared to its 9.7% monthly average from January to August. Overall market activity remained robust, with 3.53 million ACCUs traded across spot, forward and derivatives markets - broadly in line with recent monthly averages.

The Safeguard Mechanism Credit (SMC) market recorded limited activity, with 20,000 credits traded mid-month at a A$0.25 discount to Generic spot levels. The tightening spread reflected ongoing price discovery in the emerging SMC market.

Policy developments dominated sentiment. The federal government’s release of the 2035 NDC and Net Zero Plan reaffirmed the Safeguard Mechanism’s central role in achieving long-term emissions targets.

Issuance softened to 1.26 million units in the latest reporting period (to August 31), down 20% from the year-to-date monthly average.

.avif)

For a comprehensive update on the ACCU market, read our monthly ACCU Market Monthly Report

Learn more about our ACCU Market Forecast Report, a method-specific ACCU market supply, demand and price forecast. This ACCU supply, demand and price forecast is available to subscribers to the Carbon Intelligence Package.

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

The New Zealand Unit (NZU) market traded within a tight range for most of September before easing NZ$1.15 month-on-month to close lower, as sellers gradually re-emerged and buying interest softened ahead of the year’s final auction.

The third quarterly NZ ETS auction once again failed to clear, with no bids received for the third consecutive time. Around 4.5 million units were offered, including rollover volumes from previous auctions, but NZUs continued to trade roughly NZ$10 below the NZ$68 auction floor, making participation uneconomic. Futures contracts across the curve also remained below the floor, with the May-2026 contract settling near NZ$66.50.

Despite the repeated auction failures, secondary market activity was largely subdued, with prices moving sideways for most of the month and liquidity remaining thin across both spot and futures platforms.

.avif)

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

The end of September marked the UNFCCC's revised deadline for all countries under the Paris Agreement to submit their third Nationally Determined Contributions (NDCs), setting out 2035 emissions reduction targets.

Despite an extension from the original February 2025 deadline, over two thirds of parties are yet to submit. China and Australia made the deadline, but the EU has not.

NDCs submitted are projected to cut 2 billion tonnes of CO2e by 2035 – whereas 31.2 billion is needed to be cut to limit global warming to 1.5C.

Among APAC countries that have submitted their 2035 NDCs, half have indicated they will definitely use Article 6 mechanisms to meet their NDC. The table below provides a snapshot of the region’s targets.

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

In a press release by Singapore’s Ministry of Trade and Industry, the government announced that it will contract 2.18 million nature-based credits worth over $60 million from four projects in Ghana, Paraguay, and Peru as a result of a request for proposal (RFP) launched in September 2024 to meet Singapore’s 2030 NDC.

To further support its Internationally Transferred Mitigation Outcomes (ITMO) procurement, Singapore recently signed an Implementation Agreement with Vietnam, bringing the total to 9 countries from which international credits can be sourced to meet Singapore’s carbon tax obligation.

Information on the process for authorisation of these carbon credits projects and eligible carbon crediting methodologies under the Implementation Agreement are yet to be published.

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

The voluntary carbon market showed tentative signs of recovery in September, with headline indices diverging but sentiment improving.

Issuance surged, led by a strong month for Gold Standard projects. Across the five major registries, total issuances outpaced retirements by 19 million, bringing the cumulative 2025 surplus to 72.5 million credits. This remains below the 77.5 million surplus recorded at the same point in 2024, suggesting a gradual tightening in supply-demand dynamics.

Price divergence persisted. Premium credits such as Delta Blue Carbon (VCS 2250) and Vichada Climate Reforestation (GS 4221) traded near US$31.00 and US$24.00 respectively, while older REDD and renewable energy credits continued to trade below US$1.00. Market data show growing demand for higher-quality assets, with BBB-rated and above credits now accounting for 35% of retirements, up from 25% in 2022.

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

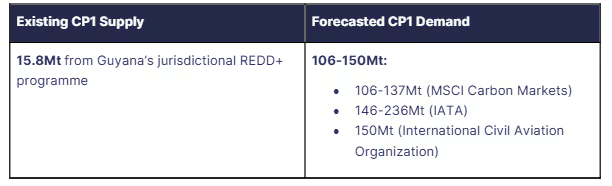

With compliance deadlines approaching and supply scarce, airlines appear to be moving towards purchases, and prices are expected to rise further absent new supply. The approval of insurance products by registries such as Verra and Gold Standard - currently being supported by Howden Insurance - would open the door to expanded supply.

Meanwhile, airlines may increasingly pursue long-term offtake agreements, structured around milestones such as Letters of Authorisation or insurance approvals, to secure access to credits.

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

As per the Sustainable Aviation Buyers Alliance SAFc registry, 8,777 tonnes of SAF linked to credits were retired in September, representing a 15% decrease from August's highs. Credit retirements were recorded in Spain, South Korea, and mostly the US led to 28,633 tonnes of CO2 abated this month, 16% lower than recorded in August.

Southwest Airlines retired the largest volume of SAF during the reporting period, totalling 5,486 MT SAF and representing 63% of the overall amount. Cathay Pacific followed with 3,000 MT SAF accounting for 34%.

All credits were generated using Hydroprocessed Esters and Fatty Acids (HEFA) methodologies, and almost all the retired credits were used to offset Scope 1 emissions abatement, with only 2% used to claim for Scope 3.

For in-depth data, analysis and commentary on international carbon markets, including macro trends, other regional markets, CORSIA and Article 6 markets, explore our Carbon Intelligence Package.

The events outlined in this month’s update highlight the evolving nature of global carbon and environmental markets and the complexity of the net zero transition.

To discuss your unique requirements, get in touch with our team today to explore how we can help.

Global Environmental Markets Report - September 2025

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.