Australia’s updated 2035 emissions target, announced in September, has set a more ambitious national course for decarbonisation. Alongside this, a series of policy developments are beginning to influence market behaviour and expectations. These shifts are reflected in the updated ACCU market forecast.

Reading time: 8 min

Quarter 3 of 2025 saw significant developments in the ACCU market.

Australia’s updated 2035 emissions target, announced in September, has set a more ambitious national course for decarbonisation. Alongside this, a series of policy developments are beginning to influence market behaviour and expectations.

These shifts are reflected in CORE Markets’ latest quarterly ACCU forecast – a central component of our Carbon Intelligence Package.

The forecast draws on fresh data, updated policy signals, and insights from across the market. The result is a scenario-based outlook that captures how supply, demand, and price dynamics are responding to changing policy and the practical realities of the net zero transition.

Keep reading to learn:

The CORE Markets’ Carbon Intelligence Package brings this complexity into view - combining method-specific price forecasting, real-time data, analytical tools, and in-market expertise in one subscription.

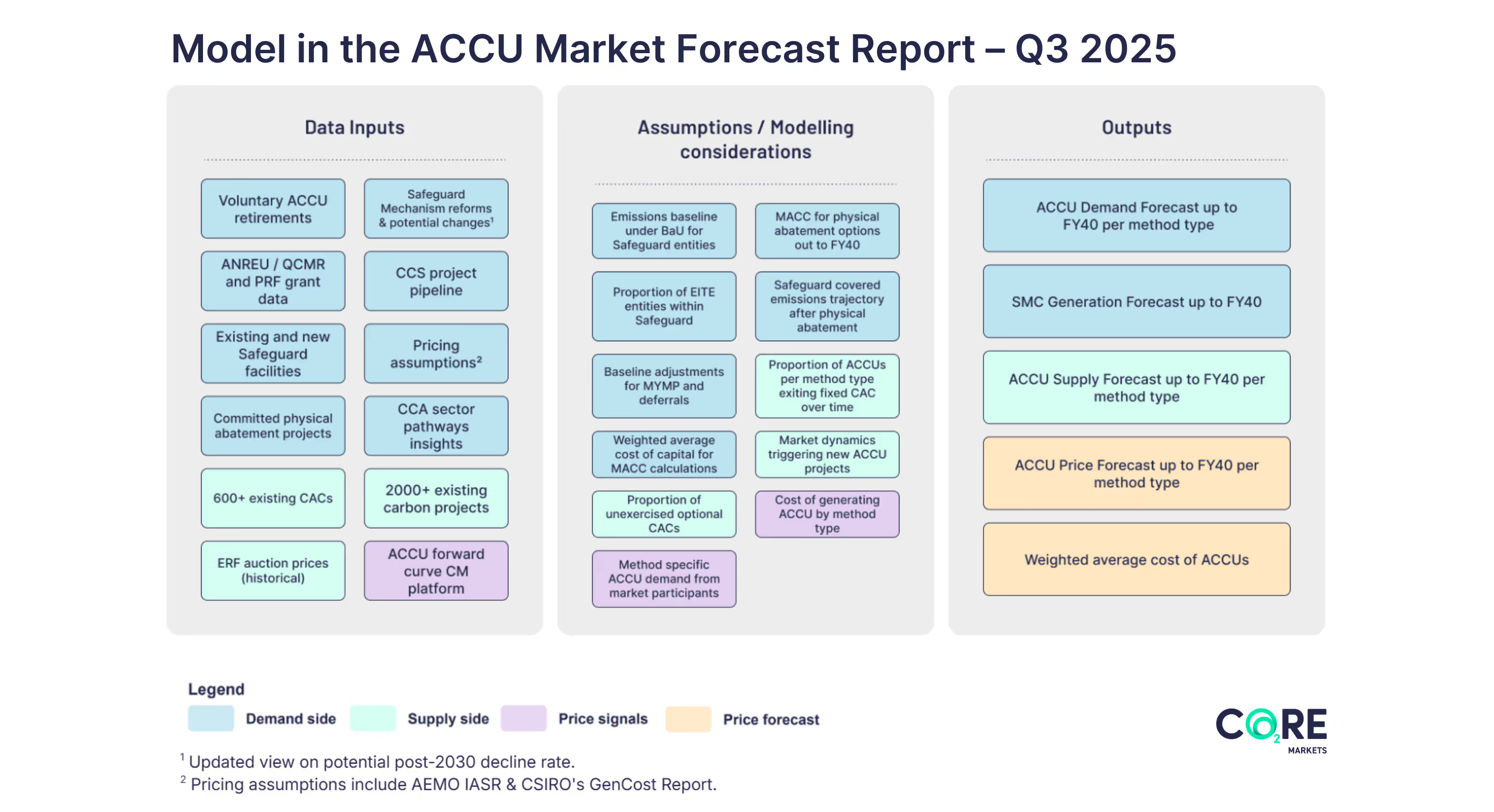

The Q3 model reflects several important updates across policy, supply and demand assumptions. These changes reflect new public data, emerging project trends and a clearer national emissions trajectory following the announcement of Australia’s 2035 NDC target.

A key shift this quarter is a refined assumption on post-2030 Safeguard baseline decline rates.

While the final settings remain subject to the Safeguard Review, Australia’s 2035 NDC to reduce emissions by 62-70% from 2005 levels provides a clearer policy signal.

In this quarter’s release, we evaluate the impact of a steeper post-2030 SGM decline rate - aligned with Australia’s NDC - on the long-term ACCU demand, particularly between 2030 and 2035.

Additional updates include:

Together, these updates sharpen the long-term outlook.

The revised Safeguard baseline decline rate assumptions materially influence the timing and scale of expected ACCU demand, while supply-side adjustments improve visibility of potential constraints and the role of new project development across the 2030s.

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

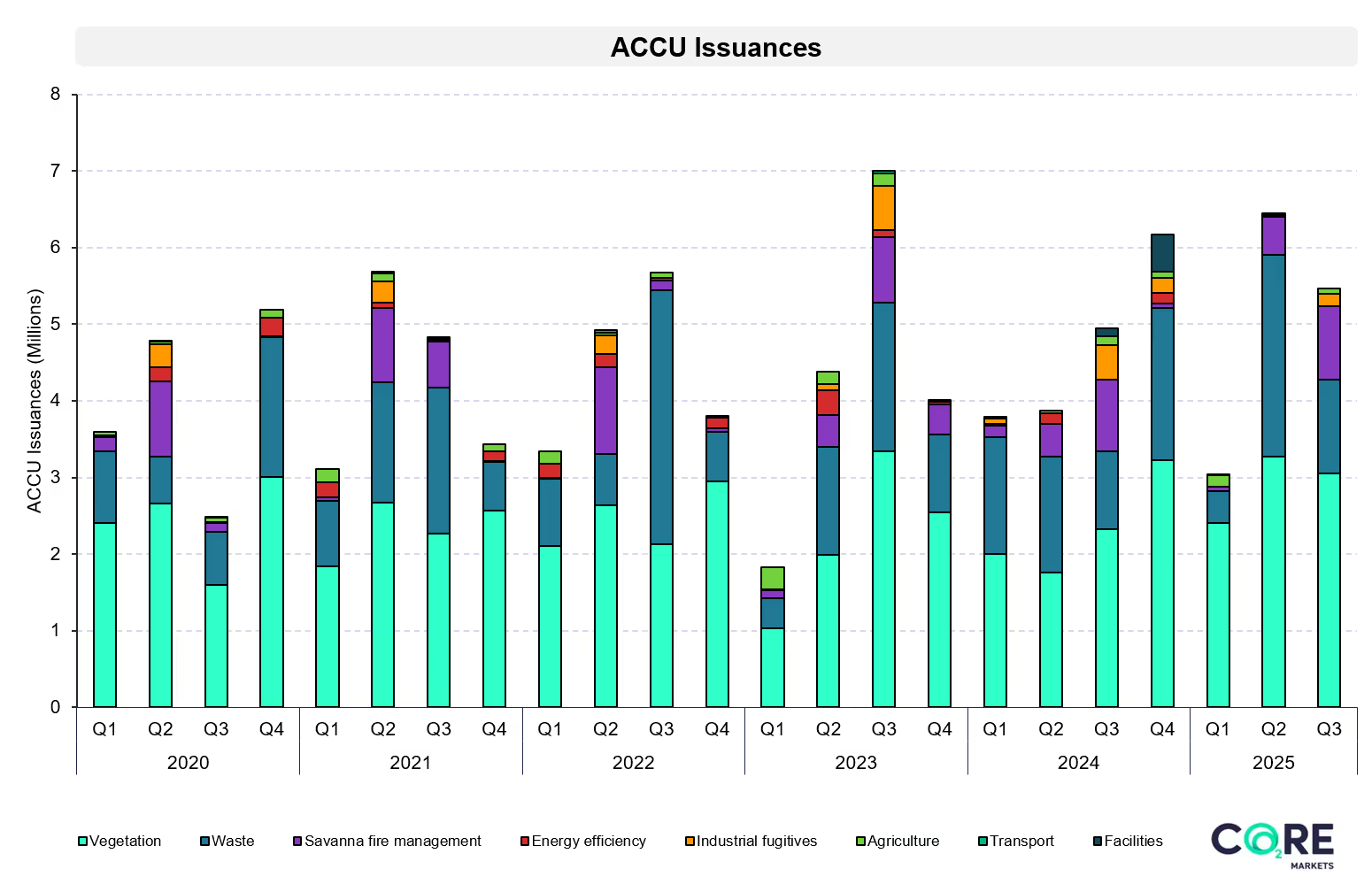

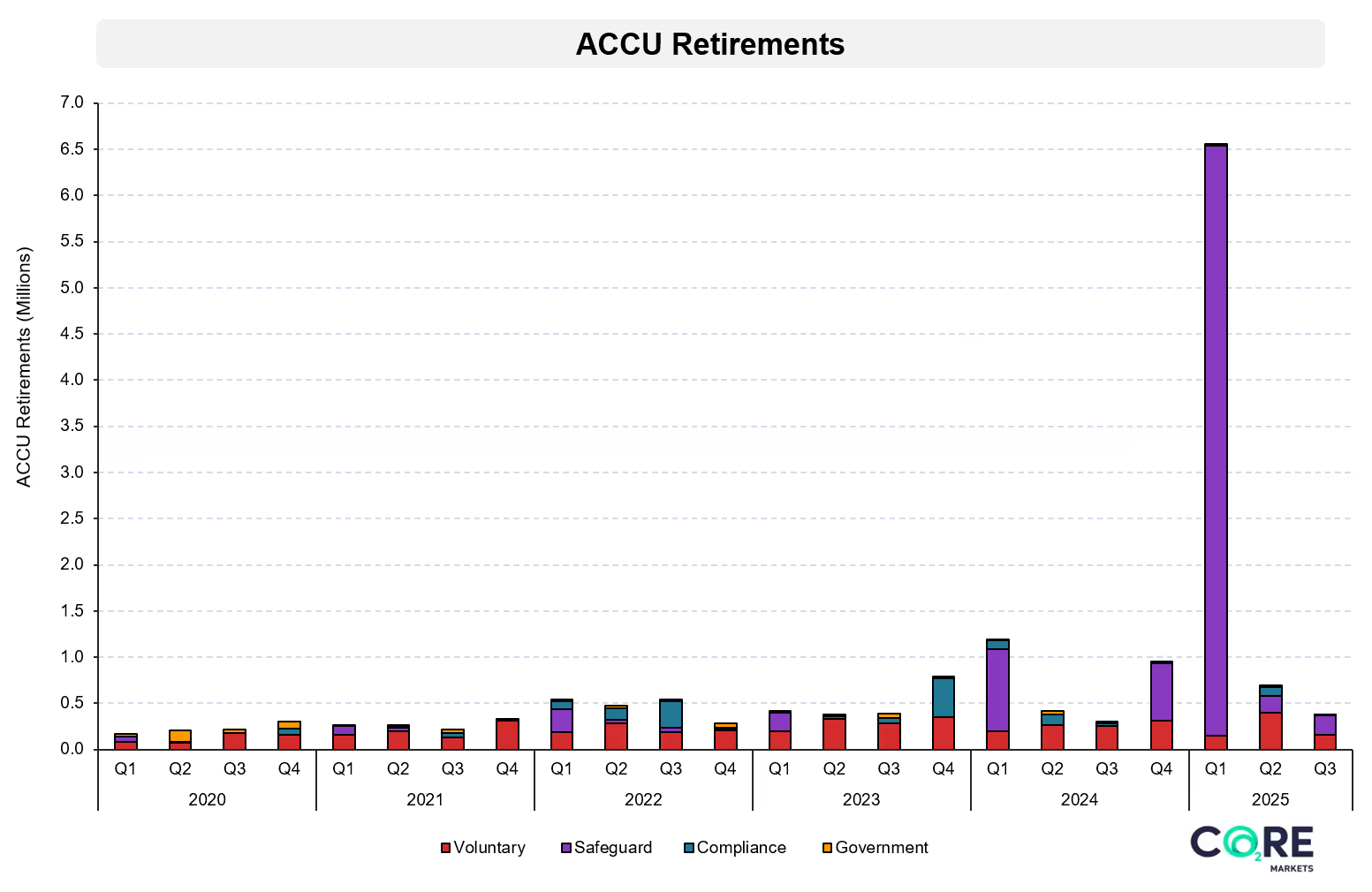

Q3 activity reflected stronger positioning from compliance buyers, softer voluntary demand and ongoing shifts in project activity.

Key public signals include:

Overall, the quarter showed a mix of stronger compliance positioning and moderating voluntary procurement.

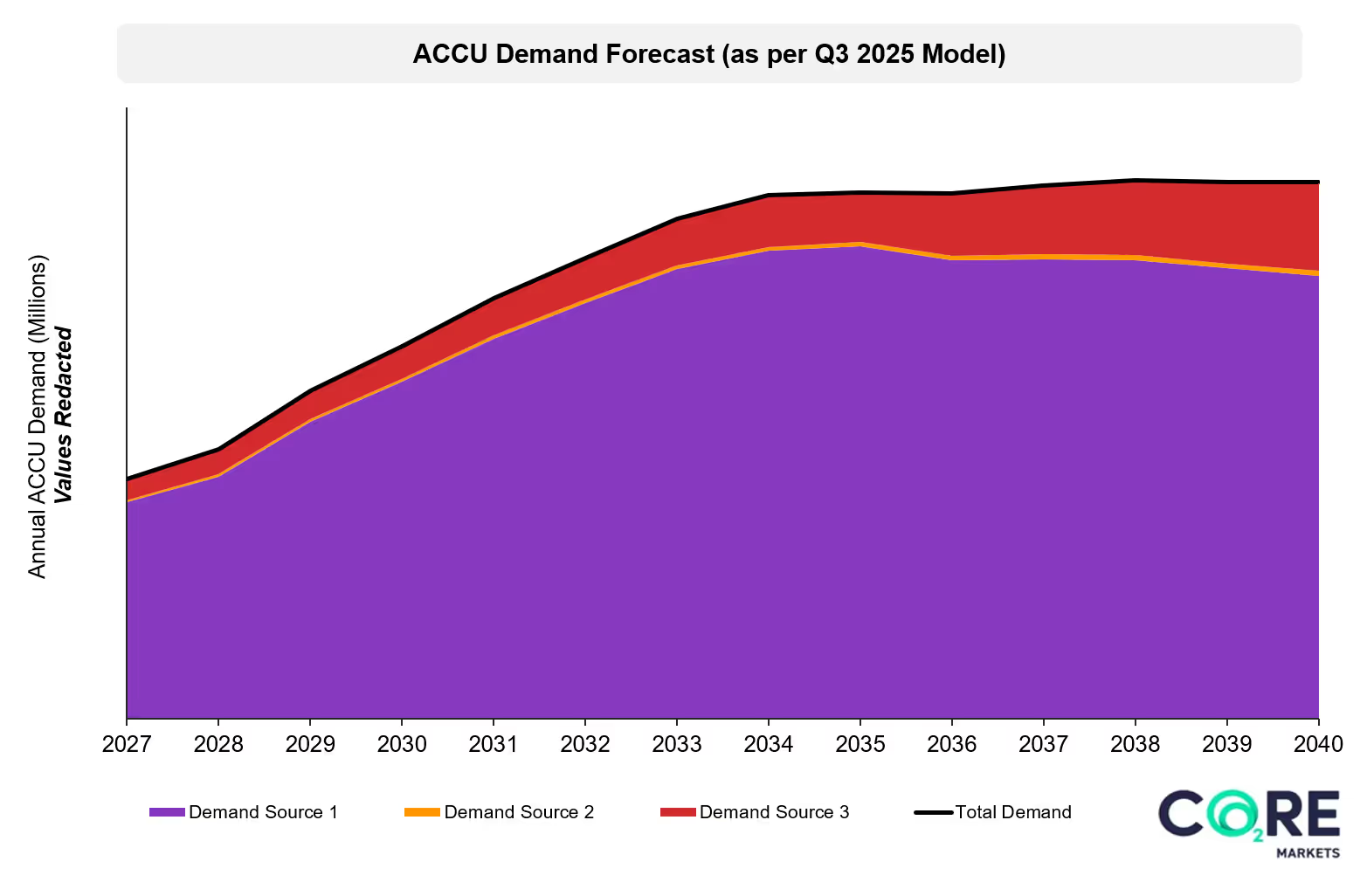

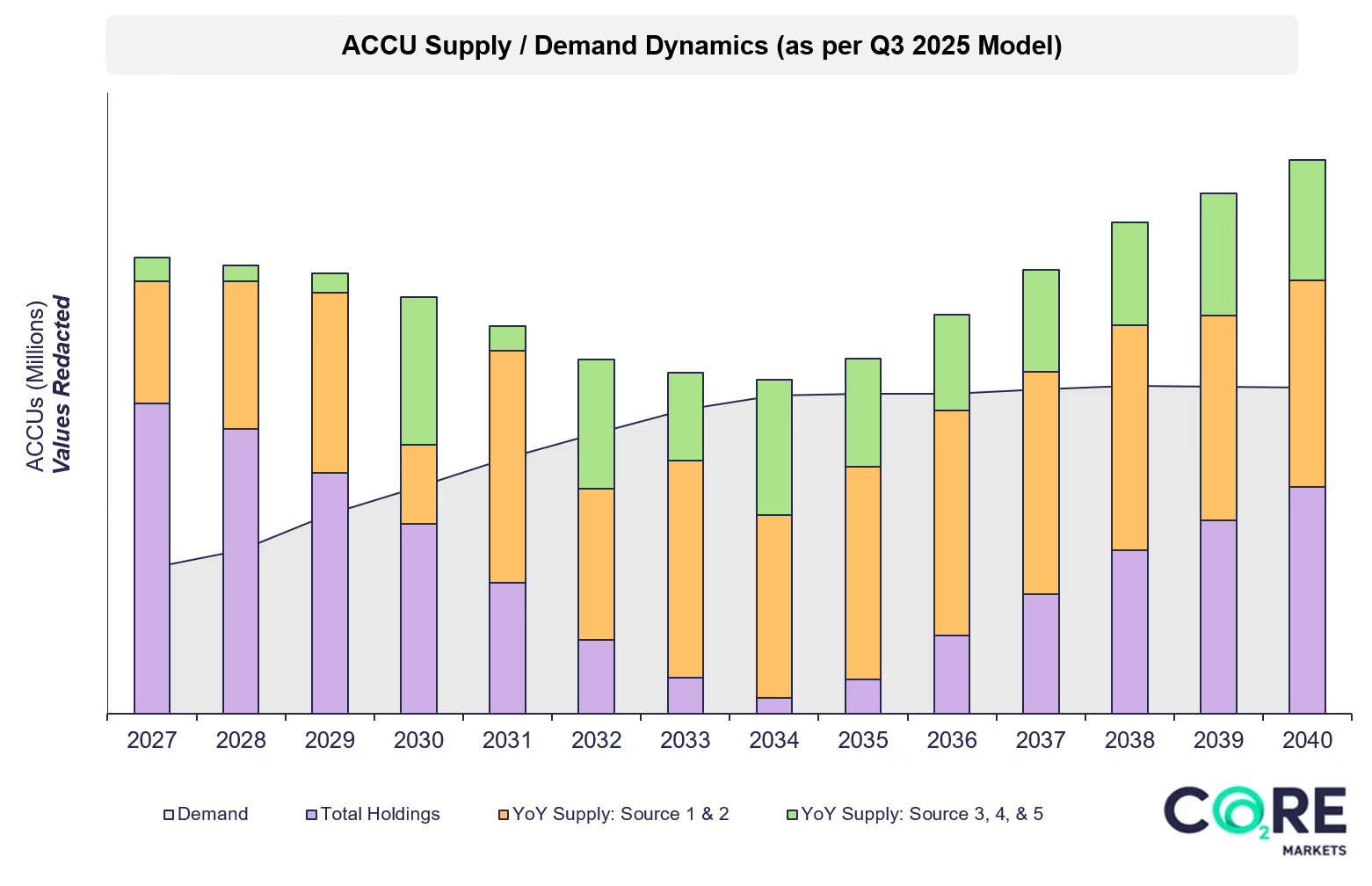

The model continues to show the Safeguard Mechanism as the dominant source of ACCU demand, supported by smaller but meaningful contributions from voluntary and state-led procurement.

Updated policy assumptions, including a steeper post-2030 baseline decline rate, shape how demand evolves across the forecast horizon.

Key modelled insights include:

For more data and market commentary, explore our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

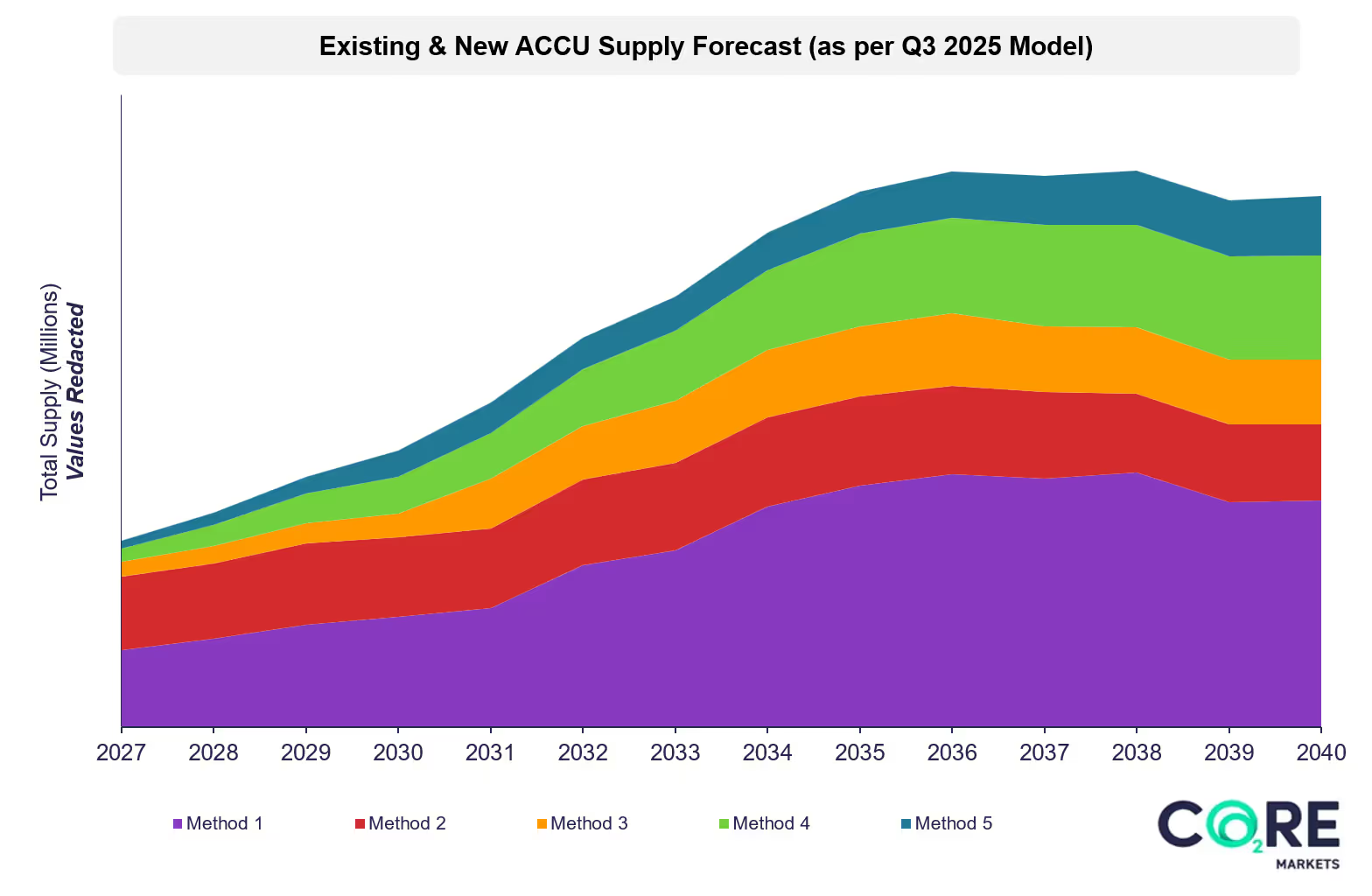

The supply outlook reflects the interplay between existing project output, new project development, method transitions and policy signals.

The Q3 model incorporates updated assumptions about project transitions, crediting periods and how the market is likely to respond to price signals and the influence of regulatory settings across the 2030s.

Key modelled insights include:

Together, these insights highlight the importance of timely investment in new project development and method availability, particularly as compliance requirements tighten and existing project output begins to plateau.

For more data and market commentary, explore our Carbon Intelligence Package, a digital subscription for deep market insights, cutting edge financial and physical data, advanced analytical tools and access to market experts.

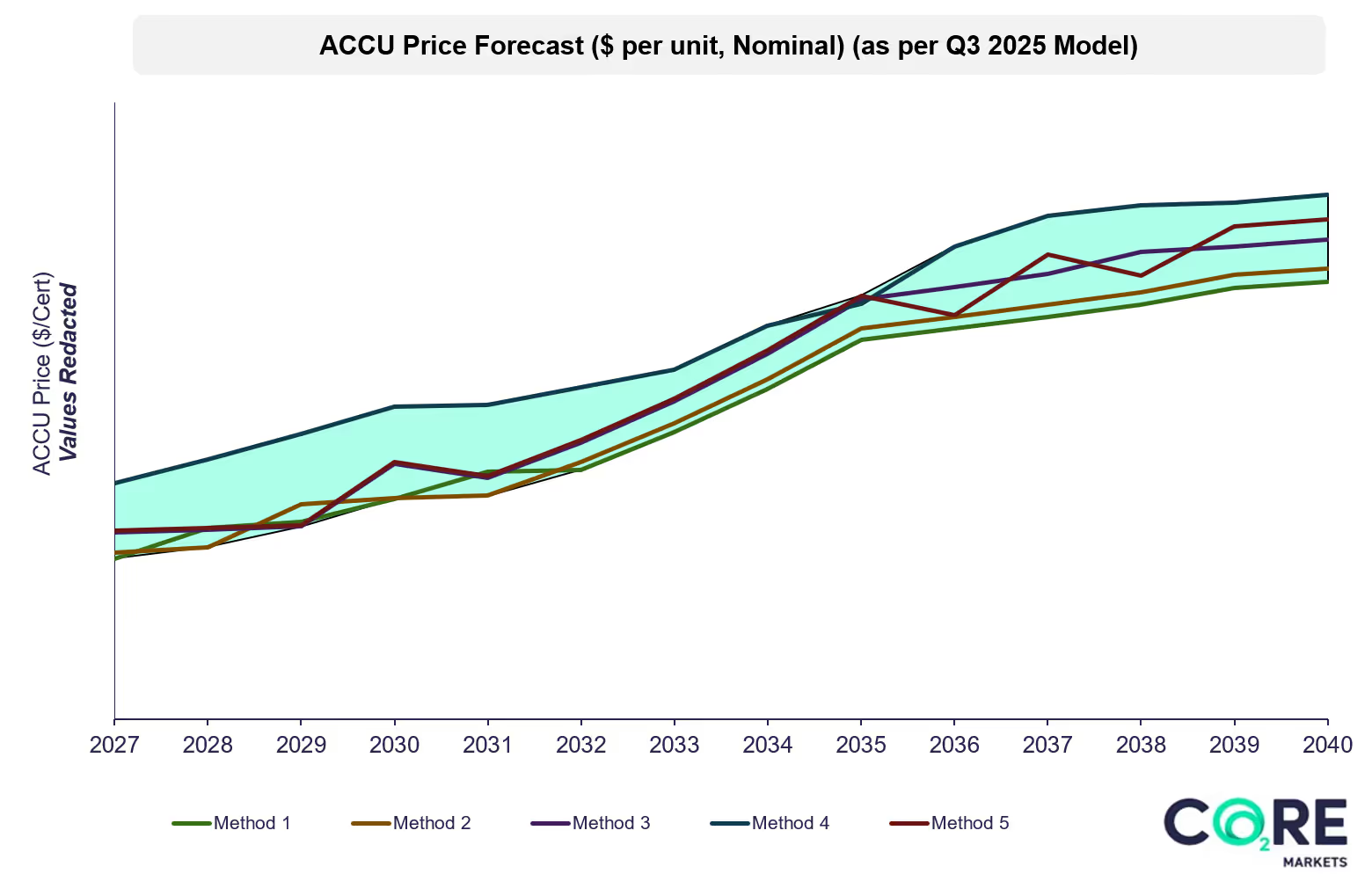

The Q3 forecast produces a wider range of potential price outcomes across ACCU method types, reflecting increased uncertainty across both supply and demand.

Price trajectories in the model are shaped by the interaction between evolving compliance requirements, the timing of new project development and changing buyer preferences.

Key modelled insights include:

Overall, the Q3 model highlights the need for buyers and project developers to plan for a broader distribution of price outcomes, particularly as long-term policy settings and supply development timelines continue to evolve.

The Q3 market forecast provides a clearer view of how updated policy signals, project activity and market behaviour are shaping long-term ACCU market dynamics. The model signals stronger potential demand, a greater dependence on new supply in the 2030s, and a broader distribution of price outcomes, reflecting rising uncertainty in the supply–demand balance.

The key message for market participants, is that long-term planning now requires a closer understanding of how policy, supply development and buyer behaviour interact across multiple scenarios.

The Q3 2025 ACCU Forecast is part of CORE Markets’ Carbon Intelligence Package – a digital subscription that integrates the quarterly forecast with live market prices, analytical tools and deep market insight. It is designed to help participants make informed decisions and align procurement, investment and compliance strategies in a changing market.

Signals and shifts: What Q3 2025 reveals about Australia’s ACCU market

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

.jpg)