Australia’s carbon market is maturing - and in Q1 2025, clear signals of this have emerged. These signals, and their implications, are captured in CORE Markets’ latest quarterly ACCU supply, demand and price forecast.

Reading time: 10 min

Australia’s carbon market is maturing - and in Q1 2025, clear signals of this have emerged.

Increased data transparency on both the demand and supply sides of the ACCU market have recently come into effect, offering greater visibility into the future of the market - and how supply, pricing and participant behaviour are likely to evolve.

A noteworthy development in Q1 was the Clean Energy Regulator’s release of Safeguard Mechanism Credit (SMC) allocations. This data provides the market with new insights into how large emitters are managing compliance obligations and physical decarbonisation, bringing Australia’s scheme incrementally closer to mature frameworks like the EU ETS.

These signals, and their implications, are captured in CORE Markets’ latest quarterly ACCU forecast update - a key part of our Carbon Intelligence Package. Updated quarterly, the forecast incorporates fresh data from our carbon analytics platform, registry activity, and inputs from an expert advisory group.

The forecast helps market participants make sense of what’s shifting - and why it matters.

Keep reading to learn:

The Q1 edition includes several key enhancements to how we model ACCU demand and supply (both from existing and new projects).

Demand-side updates:

Supply-side updates:

Modelling enhancements:

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

Informed by the recent SMC issuance data from the CER, CORE Markets has modelled the SMC issuance landscape through to FY40. While these issuances do not change the peak ACCU demand, they affect the timing of demand peaks - now forecasted to shift from FY32 to FY35.

The CER has also released a list of entities granted TEBA status and this has clarified the extent of discounted baseline decline rates, particularly in the manufacturing sector. These updates provide greater precision around forecasted demand from Safeguard entities.

From FY35 onward, we expect Safeguard-related demand to stabilise as lower-cost, technologically mature decarbonisation solutions become more viable. Therefore, liable Safeguard entities are likely to prioritise direct abatement over ACCU retirement.

Voluntary demand, by contrast, is projected to grow steadily from FY30 this increase is driven by:

Procurement behaviours remain distinct. Safeguard entities focus on cost efficiency, while voluntary buyers continue to align their procurement approaches with broader ESG narratives - favouring sequestration methods with perceived permanence, verifiability, and co-benefits.

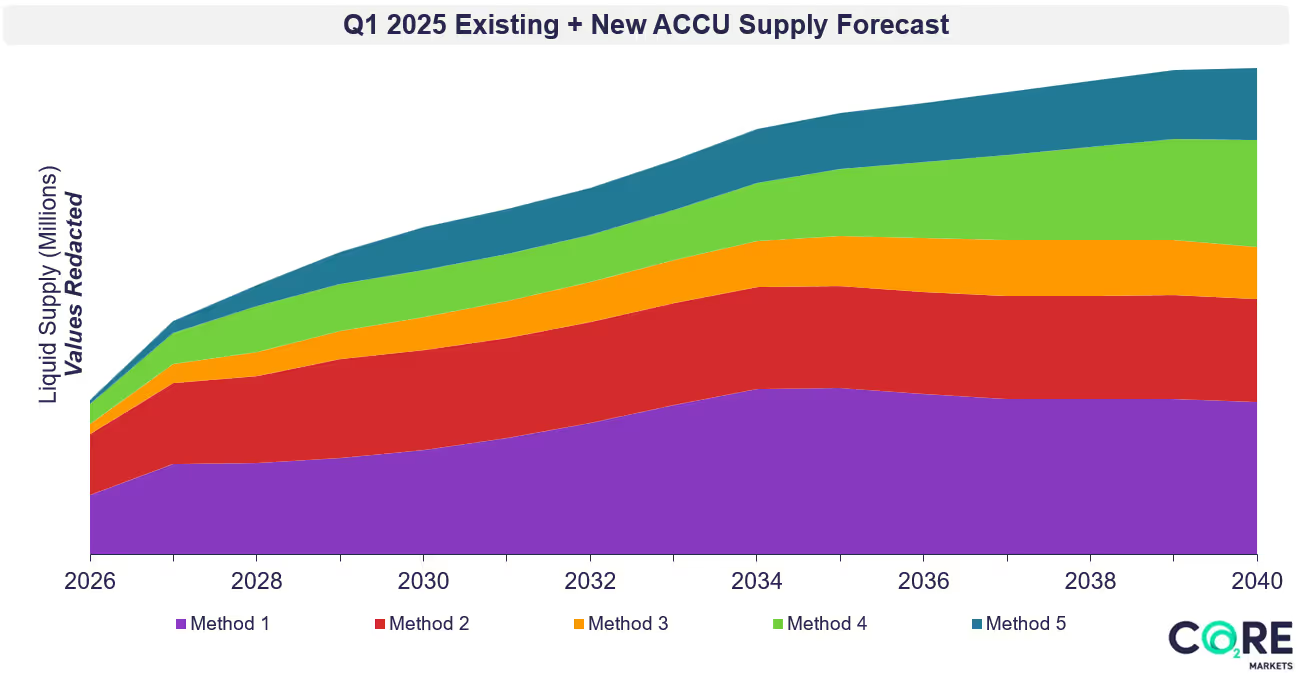

Most ACCU issuances come from a few dominant methods - primarily HIRs and landfill gas - but the pipeline is beginning to diversify. As demand grows and preferences shift, the composition and responsiveness of new supply will become more important.

Our models indicate that expected issuances from existing projects and current holdings, is sufficient to meet demand through to FY31. However, issuances from new projects are required by FY31 to cater to the demand.

We forecast that an increasing share of new issuances will come from nature-based removal projects, particularly Environmental Plantings, although these tend to carry higher upfront capital investment costs and longer lead times.

The evolution of demand - including the divergence between low-cost compliance needs and high-integrity voluntary preferences - will impact the price, supply elasticity, and attractiveness of different ACCU types.

These dynamics are likely to trigger the next wave of project development and influence the broader shape of the ACCU market between FY26 and FY40.

Australia’s ACCU market isn’t one market - it’s many.

Yet, many public discussions continue to treat ACCUs as a single, undifferentiated unit.

CORE Markets’ price forecast by method reflects that different units carry different forms of value - whether due to higher generation costs, integrity characteristics, or co-benefits beyond carbon.

Built using method-level data and real-world market signals, our model accounts for:

The result is a scenario-based forecast that better reflects the complex reality of Australia’s carbon market. Developed by our Advisory team and peer-reviewed by a specialist industry group, it forms part of CORE Markets’ Carbon Intelligence Package.

Australia’s carbon market is entering a more signal-rich phase - but navigating it still requires interpretation.

As compliance markets evolve and voluntary preferences shift, market participants need more than a headline price. They need insight into what’s driving demand, where supply is emerging, and how policy, preference, and performance intersect.

The Q1 2025 ACCU Forecast helps decode these dynamics — not just for today’s procurement, but for long-term positioning.

The Q1 2025 ACCU Forecast is part of CORE Markets Carbon Intelligence Package - a decision-support tool for organisations with exposure to Australian and global carbon markets.

To learn more or request access, contact our team.

Signals, shifts and scenarios: What Q1 2025 reveals about Australia’s ACCU market

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

CORE Markets has launched Asset Intelligence, connecting renewable project data with power market context, commercial analysis, forecasting and risk modelling to support stronger asset and portfolio decisions.