The latest edition of our monthly Australian Energy & Environmental Market Update is now available. Keep reading for energy and environmental price movements, policy updates and other news.

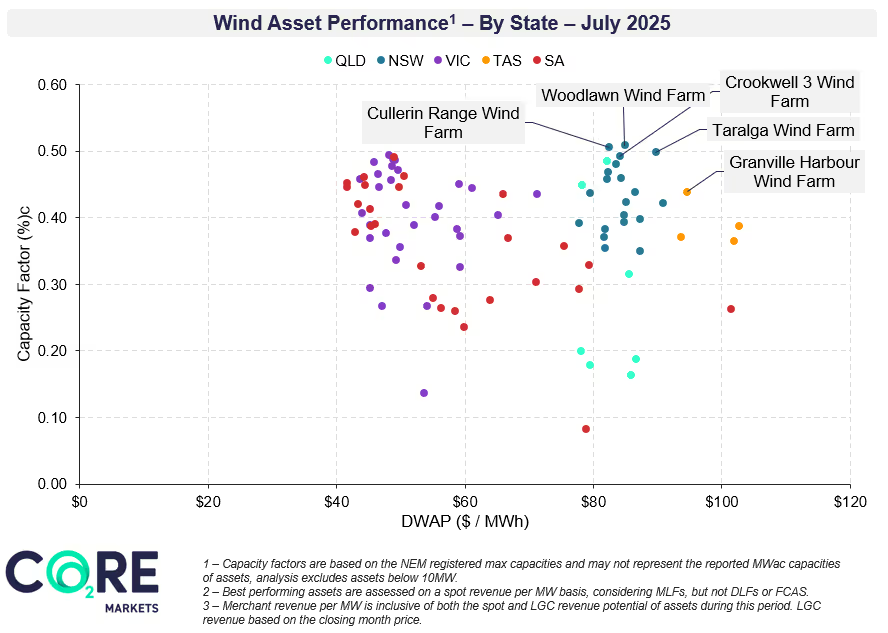

This month’s update covers July’s spot market trends, with higher renewable energy penetration across all NEM regions, contributing to a decline in prices from the elevated levels in June. We also cover wind asset performance, highlighting the top performing assets that took advantage of the strong wind generation across the NEM.

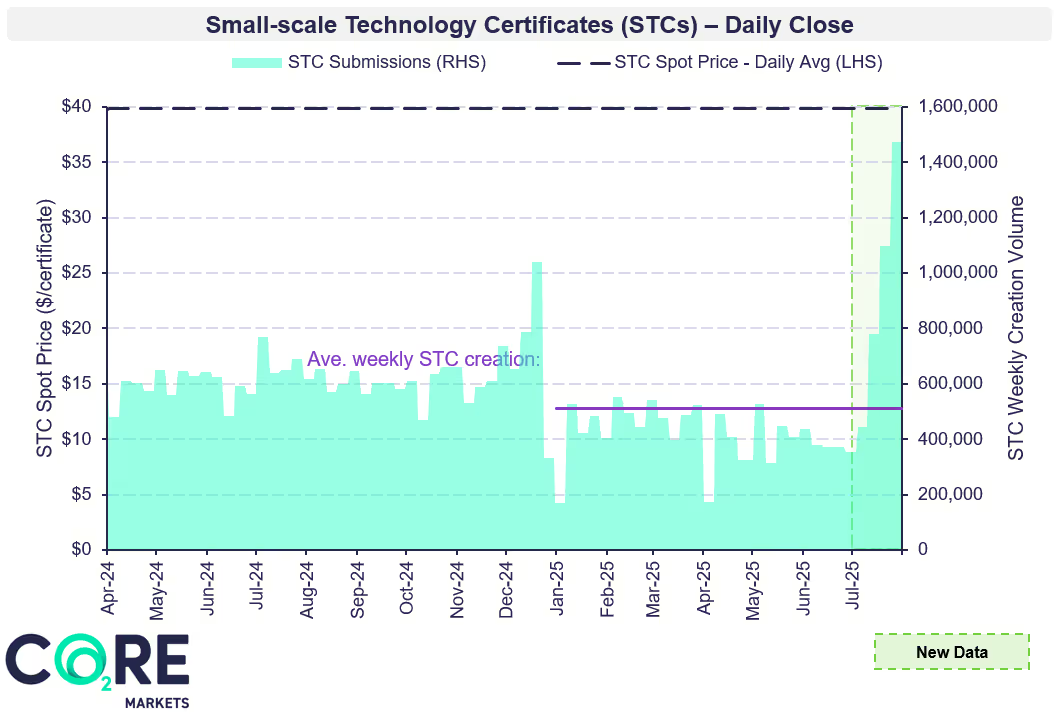

In the environmental markets, we highlight the surge in STC creations this month, driven by the Cheaper Home Batteries Program. This program is featured in our news highlights, along with details of the updated Capacity investment scheme (CIS), the release of the 2025 enhanced locational information and the final 24-25 GenCost report.

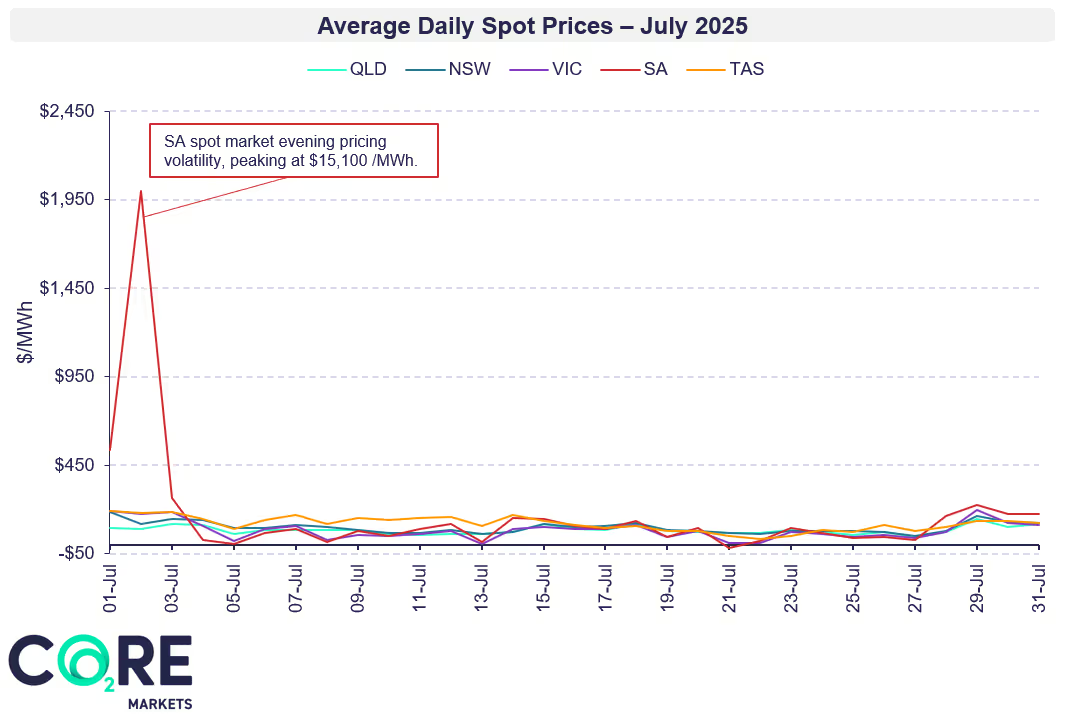

This month the electricity spot market experienced a sharp decrease in monthly average prices across all NEM regions, following last month’s record high, when prices exceeded a $200/MWh monthly average. NSW and VIC saw the steepest decline, decreasing over $150/MWh and $180/MWh, respectively.

Relative to last month, the number of high price intervals (above $300/MWh+) softened across the NEM while negative price intervals increased in frequency recording an increase of 2,343 negative intervals across the NEM

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.

NEM-wide Variable Renewable Energy (VRE) penetration increased by 4.26 percentage points from last month, rebounding from the June decrease to land above May levels. This was primarily driven by a NEM wide increase to wind generation, with individual state-based wind penetration increasing from 1 to 5.3 percentile points month-on-month depending on the region.

Each month we feature a different asset type - rotating between coverage of solar, wind and BESS projects. This month's focus is wind asset performance.

Looking for more in-depth renewables asset analysis?

Learn more about our Renewable Energy Offtake Market Report, an important and recurring pulse check for renewable energy buyers and seller.

Log in to the CORE Markets platform for more data, insights and commentary. Don’t have an account? Learn more

Looking for ACCU coverage? Read our ACCU Market Monthly Report here.

This month the energy market eased from the elevated levels experienced in June, with both spot market and futures seeing relatively subdued pricing for July, although SA still experienced periods of extreme volatility early in the month. Wind assets saw increased generation, lifting capacity factors for most assets.

For asset owners and market participants, understanding key seasonal trends in the market highlights the importance of strong market knowledge and effective hedging strategies to manage the impact of seasonal variations and maximise revenue opportunities.

The CORE Markets team partners with renewable energy developers and corporate buyers to manage market risks. Get in touch to explore how we can support your energy market approach.

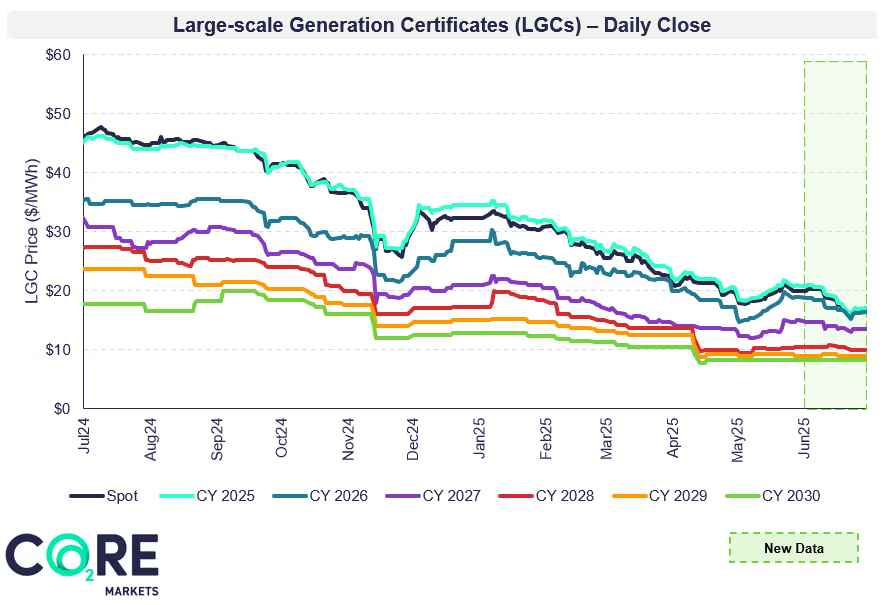

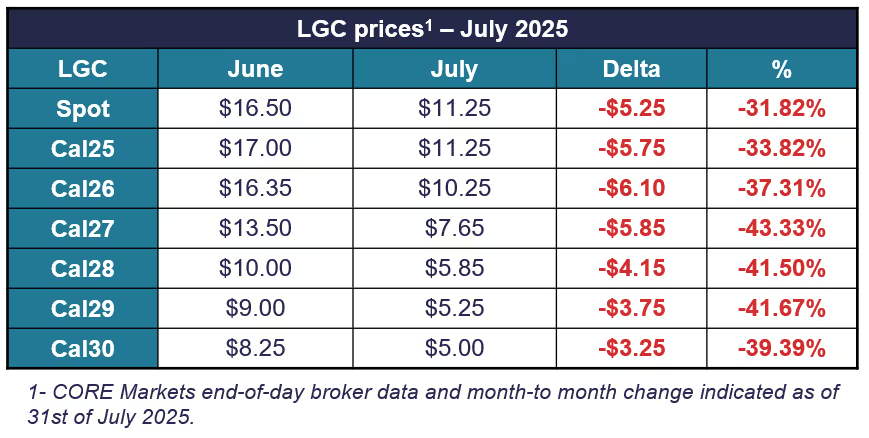

LGC market activity declined again this month, with both spot and forward prices falling. STCs showed a surge in creation activity, with a weekly increase exceeding1 million certificates, driven by the Cheaper Home Battery Program. Staying ahead of new programs and regulator changes is key to guiding procurement strategies to take advantage of opportunities and keep costs low.

The CORE Markets team supports demand and supply side market participants in navigating these markets – across strategy, procurement and trading execution. Get in touch to learn how we can support your goals.

The events outlined in this month's update highlight the evolving nature of energy and environemental markets and the complexity of the net zero transition.

To discuss your unique requirements, get in touch with our team today to see how we can help.

Australian Energy & Environmental Market Update - July 2025

Log in or register a free CORE Markets account to get closer to power, environmental and carbon markets with insights and updates from our experts.